JP Morgan AM: Korea corporate reforms could take hold quicker than Japan

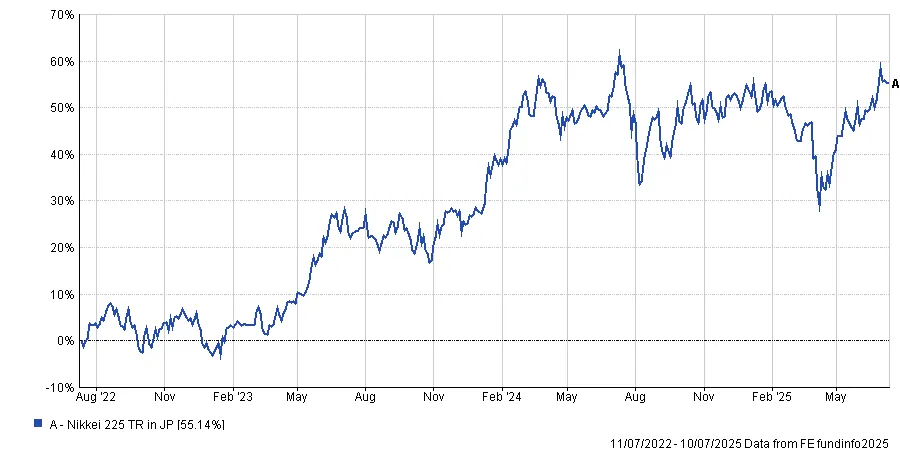

The Korean corporate governance reforms could transform its stockmarket faster than the Japanese corporate governance reforms which took off two years ago, according to Alexander Treves (pictured), head of investment specialists for APAC equities at JP Morgan Asset Management.

Firstly, reflecting on progress in Japan, Treves said: “The Japanese corporate governance revolution has got so much momentum that we’re very confident that the genie’s out of the bottle,” as reported in our sister publication FSA.

“It took a while to gather that momentum, but if we look at the magnitude of share buybacks, at different payout rates, at diversity of board structures, board composition, et cetera, all of that is looking better than ever.”

“We’ve got this combination of better corporate governance, which argues for higher multiples, and a more sustainable inflationary and economic growth story, which is really interesting.”

While reforms in Japan began as early as 2014 with a new stewardship code and a new corporate governance code a year later in 2015, it wasn’t until 2023 that the Tokyo Stock Exchange started putting pressure on its listed companies.

Japanese stocks then emerged from a decades-long slumber to breach all-time highs in 2023 and again in 2024.

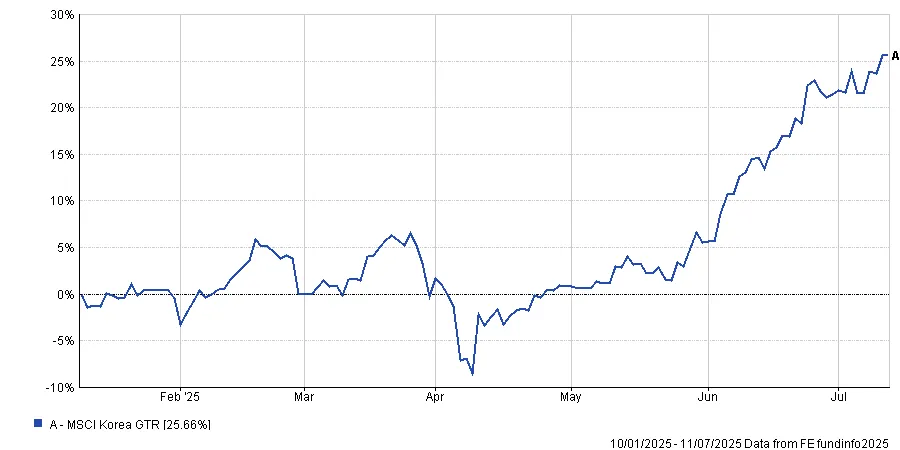

When it comes to South Korean stocks, it may not necessarily take a decade for its stockmarket to be revitalised by corporate governance reforms.

South Korean stocks have rallied over 40% in the past three months as investors started to price-in the recently passed landmark amendments to its commercial act aimed at strengthening shareholder rights and corporate transparency.

After the South Korean political upheaval rattled investors late last year, the new government’s proposed reforms seems to have helped push its stockmarket to become one of the best performing indices globally year-to-date.

According to Treves, Korea is a position to move a little bit quicker than Japan on its corporate governance reforms.

“There is political momentum to enact further change,” he said. “We think the new administration is doing a good job there and we think they’re keen to be seen to be making further progress rather than resting on their laurels.”

“I think there is a little bit of a sense of competition between Korea and Japan,” he said. “I think Korea’s looked at what’s happened in Japan and thought, ‘that’s quite a good idea’.”

Additionally, South Korean stocks are still under-owned by foreigners in his view, and despite its 40% rally, they are still not yet expensive.

Indeed, the MSCI Korea index trades at a 9.7 forward price-to-earnings ratio versus the MSCI AC Asia ex Japan index at 13.6, and the MSCI Japan index at 14.8.

In an environment where investors are looking to diversify their US exposure, Treves said Asia more broadly is likely a natural destination.

“We have been through a period where I would argue too much investor attention has been focussed on the US,” he said.

“I will fully acknowledge that there are a lot of great companies in the US, and I totally get that the US is really ‘good at capitalism’ but that doesn’t mean that you should have all of your assets in US equities, nor does it mean that you should be insensitive to valuation.”

He added: “You’ve always got to ask yourself for any given asset class, who is the marginal buyer. I think we can make the argument that pretty much everyone already owned US equities.”

This article originally appeared in our sister publication, Fund SelectorAsia